Module 10B: Introduction to Woodlot - Income Tax and Estate Planning

Lesson Two - Business Types

Business Entities

The three most common types of business structures (sometimes called business entities) are proprietorships, partnerships, and corporations. Each of these has unique legal and income tax features.

Proprietorship

A proprietorship is a business carried on by an individual. The individual is the owner, in charge of and ultimately responsible for all activities of the business. The owner assumes all the risks and does not share the profits or losses. Profits are calculated after deducting reasonable expenses. There is no legal difference between the individual and the proprietorship. If the business fails, the individual’s personal assets may be subject to seizure by creditors.

For income tax purposes, the business income and losses get added to the individual’s income from other sources. The proprietor is taxed on the net income, not based on cash drawings from the bank account. Tax is calculated on taxable income at graduated personal income tax rates.

Lumping income and losses from different sources together allows the individual to deduct losses against other forms of income, such as employment or investment income. This may be a big advantage during a business start-up period, when there are often losses.

If business losses exceed income from all other sources in a particular year, the excess may be carried back to recover tax previously paid or carried forward to reduce future taxable income. See Appendix 2 for details on the allowable carry-over period.

You should note that use of the word loss or losses refers to the situation where deductible expenses exceed revenues. It does not necessarily include the situation where a woodlot owner suffers an economic loss due to a natural event such as fire, hurricane or insect damage. Under these circumstances, the taxpayer might be entitled to a write-off only if there are previously undeducted costs associated with the woodlot. Such a write-off would not be available for any costs attributed to the underlying land.

When the owner sells or otherwise disposes of the business assets – for example, by transfer to family member, deemed disposition on change-of-use from business to personal use, or deemed disposition on death; then business income or losses may result as well as capital gains or losses.

Partnership

A partnership is an agreement between two or more parties to combine resources, credit, and expertise to carry on business together in order to earn a profit. Although the partnership possesses assets and property of its own, it is not a separate legal entity from the partners. Each partner is fully responsible for the debts and business obligations of the partnership. If the business fails, each partner’s personal assets may be subject to seizure. Although a written contract is not necessary, a signed partnership agreement is highly recommended. This agreement should set out the rights and obligations of the individual partners, including but not limited to:

- income sharing entitlements

- financing or capital requirements

- property to be contributed

- personal involvement requirements

- admission and departure of partners

- dissolution of partnership

A partner who contributes a particular asset to a partnership would not necessarily receive the asset back if the partnership is dissolved unless it is written into the partnership agreement or otherwise agreed to by the partners.

For income tax purposes, the partnership calculates its taxable income and allocates this amount among the partners. A partnership does not file its own income tax returns. Each partner includes his share of income or loss on his personal income tax return. (Again, the amount of cash drawn from the partnership’s bank account by a partner does not factor into the partner’s income.) The result is the same as if each partner were a proprietor who had earned that much income or suffered that much loss. The loss carryforward and carryback rules are the same as for a proprietorship.

An interest in a partnership is a capital property that can be sold or transferred to another person, subject to terms or conditions in a partnership agreement. Any gain or loss on the sale of a partnership interest would be a capital gain or loss. The cost of a partnership interest is increased by the partner’s share of earnings and reduced by the partner’s share of withdrawals or distributions from the partnership.

On wind-up, a partnership generally disposes of all of its assets to its partners at fair market value. Business income and capital gains would be allocated to the partners. However, a rollover is available on the wind-up of a partnership where each partner receives a pro-rata undivided interest in each property of the partnership. The benefit of this rollover provision is that inherent gains in the partnership property are not taxed until some time in the future. The drawback is that the partners must hold the property (distributed on wind-up) jointly. If this is impractical for some assets, they may be distributed to particular partners before the wind-up. A similar type of rollover is available where one partner buys out the other partners and carries on the business as a proprietorship.

Corporation

A corporation is a separate legal entity, distinct from its shareholders. It may own assets and incur debts and can generally contract and negotiate on its own behalf. Shareholders are not responsible for the debts of the company unless they have provided personal guarantees. Private companies are usually set up under the laws of a province, although federal incorporation is available. The incorporating statute will impose some formalities on the company, such as the need to hold meetings, elect directors and officers, and so on.

For tax purposes, a corporation calculates its own taxable income and files its own tax return. You can see from Appendix 3, a company in Nova Scotia pays tax at a favourable provincial rate on its first $400,000 and a favourable federal rate on its first $500,000 of business income earned in a particular fiscal year. If the business is profitable and generates more income than the shareholders need for personal living requirements, this difference in tax rates is a big advantage to incorporation. The tax savings provide additional funds to finance growth or reduce debt. However, this difference in taxes is actually a deferral of tax. There is a second level of taxation when the retained earnings of the company are eventually distributed to the shareholders. Nevertheless, this tax bill may be postponed indefinitely, as long as the profits stay in the corporation.

The shares of certain qualifying corporations are eligible for a $750,000 capital gains deduction on their disposition. There are tests to be met, but as long as substantially all of the company’s assets are used in the business, the shares should qualify. Other assets, such as excess cash, stock market investments, or rental properties, may create problems. The problems may be avoided with advance planning and preparation, so that the shares of many private companies will qualify. On the other hand, if the business is carried on as a proprietorship or a partnership, only capital gains on qualifying farm land, farm buildings, farm quota, and interests in family farm partnerships are eligible for the $750,000 capital gains deduction. So if the business is not farming, the $750,000 capital gains deduction can only be achieved if it is carried on through a corporation.

One disadvantage of incorporation is that if there are losses in the early years of a business, there is often no other source of income in the company against which they can be claimed. Otherwise, the loss carryover rules for corporations work exactly the same as for proprietorships and partnerships.

On the wind-up of the business and distribution of the assets to the individual shareholders, the company is taxed based on dispositions of assets at market value. Shareholders will also be taxed on the amount of taxable dividends they are considered to receive. This ends the tax deferral advantage of incorporation we mentioned earlier, which is why corporations often carry on as personal holding or investment companies after the business activities have been wound down.

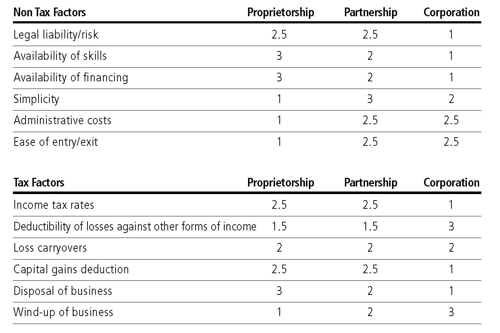

Choosing the right business entity

Choosing the right business entity will always depend on the particular circumstances of the business. Limited legal liability and lower income tax rates available through a corporation are often deciding factors, but these are offset somewhat by higher cost of administration and complexity.

The table compares the tax and non-tax factors that should help you choose a business entity. A score of one shows the advantage lies with that choice of entity. A score of three shows a disadvantage for that entity. If there is no significant difference between two or more entities, their scores have been averaged. We have tried to rank the factors in decreasing order of importance. However, the scores and the rank are subjective judgements, meant to serve as a guideline only.

Change from one business structure to another

You can generally start a business operation as a proprietorship and transfer the business assets to a partnership or a corporation at a later time without immediate tax consequences. Usually, you can also incorporate a partnership without tax consequence or, as mentioned before, one partner can usually acquire the other partners’ interests in the partnership and carry on the business as a proprietor without tax consequence to the continuing partner.

There are no provisions in the Income Tax Act however, for the transfer of business assets of a company out to individual shareholders so that the business can be carried on as a proprietorship or partnership. Such a transfer can rarely be made without tax. Transfers of business assets between companies can often be achieved without income tax effect.

Although switching between business entities is often feasible, it is certainly a complex area from an income tax point of view. There are many technical traps to avoid and many planning opportunities that should be considered, such as estate planning, income splitting, creditor protection, and so on. Remember that the purpose of “switching” is to achieve long-term advantages. Up-front costs should be evaluated like any investment undertaken by the business. Professional assistance is a must.

Ranking of business entities based on tax and non tax factors. (Actual Nova Scotia Marginal 2009 tax rates are found in Appendix 3.) A lower score implies an advantage lies with that business entity for that particular tax or non-tax factor. A higher score implies a relative disadvantage. If there is no significant difference, scores have been averaged.

The above tables are meant to assist a woodlot owner in reflecting on factors that are most relevant to their situation. The rankings are subjective and may change based on individual circumstances.

Special Farm Rules

There are several special income tax provisions that are applicable to farmers.

Cash Basis Accounting

Non-farm business income is normally measured using the accrual basis of accounting, however farmers can choose to report on the cash basis.

Once you choose to file your tax return using the cash basis, you can only switch to the accrual basis of accounting with the approval of CRA.

If you use the cash basis, you only use revenues for which the cash has actually been received, and expenses actually paid in the year to determine income. This lets the taxpayer reduce income by paying off outstanding bills at year-end.

Cash basis farmers do have the option of adding an amount to their income up to the fair market value of their inventory. This allows them to smooth or average income. Using these provisions they can avoid the possibility of not paying any tax in one year, and missing the advantage of the low marginal rates, followed by a year of high taxable income, some of which is subject to the top marginal rates. The provision may also be used to increase income and take advantage of old losses that might otherwise expire.

Loss Carryovers

See Appendix 2 for loss carryovers allowed for farming losses.

Restricted Farm Losses

A business carried on with a “reasonable expectation of profit” may have losses. But where “a taxpayer’s chief source of income for a taxation year is neither farming nor a combination of farming and some other source of income,”5 the loss from farming that can be used as a deduction against income from other sources is limited to the first $2,500 of loss plus one-half of the next $12,500 for a maximum of $8,750. Any excess (known as a “restricted farm loss”) can be carried back or forward as shown in Appendix 2. Restricted farm losses can only be used to the extent of farm income in those years. In this way, the benefits from tax losses which often arise in the early years of business - and are accelerated by use of the cash method of accounting - are restricted for part-time farmers when farming if farming is not their main course of income. This is also true for an individual who combines farming with another source of income. See Appendix 1 for summary.

Whether or not farming is the taxpayers primary source of income has been the subject of endless court cases. The courts have considered time commitment, capital commitment, and expectation of profitability to be determining factors.

You need to ask:

- How much time is spent farming versus generating income from other sources?

- How much capital is invested?

- What is the gross revenue of the farming operation?

- How much farming experience and knowledge does the taxpayer have?

- What is the income potential of the farming business (as demonstrated by a business plan)?

You should note that for a hobby farm with no expectation of profit, no expenses are deductible on your tax return.

Investment Tax Credits

Investment tax credits are available to farmers and loggers in Nova Scotia for expenditures on “qualified property.” An eligible expenditure must be for a qualifying building or qualifying machinery and equipment. The asset must be new and unused at the time of purchase. Property that has been previously owned, used as a demonstrator, or leased is not eligible. The asset must be acquired to be used by the taxpayer in Canada primarily (more than 50 percent) in the taxpayer’s business of farming or logging. (Use in other industries may also qualify but that is outside the scope of this booklet.) Examples of buildings, machinery and equipment that qualify include nearly all structures, machinery and equipment used in farming or logging activities, except for cars and trucks designed for use on highways. However, logging trucks weighing more than 7,258 kilograms will qualify.

The available credit is calculated at 10 percent of the capital cost of eligible assets. The credit must be claimed within 18 months of the tax year end or it is lost.

Capital cost is the actual cost less any other government or non-government assistance received. HST recovered as an “input tax credit” is not included. The credits are available to all taxpayers regardless of size or legal structure of the business, and can be used to offset 100 percent of federal income taxes payable. If not enough federal taxes are payable against which to claim the investment tax credits, 40 percent of current year credits earned by individuals and certain corporations are refundable. A corporation will not qualify for this refund if it had - or was part of an associated group of companies that had - taxable income of more than $500,000 in the immediately preceding taxation year for years beginning after 2008 ($400,000 for 2008, $300,000 for years between 2003 and 2007). Further restrictions to the refund apply to companies (or groups of companies) with more than $10 million in assets.

Investment tax credits earned but not used to offset federal taxes payable or refunded to the taxpayer can be carried back three years and forward twenty years (for tax years after 2006, carried forward 10 years for years before 2006) and claimed against federal taxes in those years.

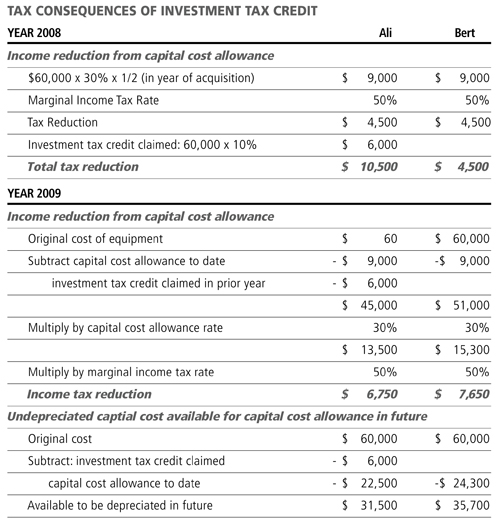

Here is an example that shows the benefit of investment tax credits. Let’s assume the following:

- Two individuals, Ali and Bert, each acquire a piece of equipment for $60,000 in 2008. Ali uses the equipment in logging (an eligible activity for investment tax credit purposes) whereas Bert uses the equipment in an ineligible activity (perhaps construction).

- In both cases the equipment can be depreciated at a rate of 30 percent for income tax purposes.

- Both individuals are earning profits and have a marginal tax rate of 48 percent.

The tax consequences are shown in the table below. You will see that claiming an investment tax credit will result in lower capital cost allowance claims in following years.

Capital Gains/Succession

In many cases, farmers receive favourable treatment on the taxation of capital gains. There are also rollover provisions for the tax-free transfer of a farming business from parent to child. We will also discuss these in more detail later.

Exercise 3

Justin has just inherited a woodlot. He decides to supplement his income from a local garage with income from the woodlot. He has decided to purchase a small tractor to use with a trailer to haul wood. In the first year of business, he spends $20,000 on a used tractor and his other costs total $7,000. His loss in the first year is $10,000 (tractor depreciation plus other costs). How much of this is he entitled to claim against his income? (see exercise 3 for answer)

Exercise 4

Raymond purchased a new skidder in 2008 at a cost of $36,000. The skidder is used in a farming business and can be depreciated at a 20% rate. Raymond has a marginal tax rate of 30%. What would his income tax reduction be for the year 2008? (see exercise 4 for answer)